Gartner

Recurring Billing

Stripe

Jake Vacovec

The recurring billing software market has reached an inflection point. According to Gartner's latest Magic Quadrant for Recurring Billing Applications, this sector generated approximately $5 billion in 2024—but the story beneath that number reveals a fundamental shift in how companies should think about their billing infrastructure.

A Market in Transition

Here's what makes this moment particularly interesting: of that $5 billion total, only about $1 billion comes from modern SaaS vendors. The remaining $4 billion? Legacy on-premises systems, primarily serving telecommunications, financial services, and utilities companies that have been locked into expensive, inflexible solutions for decades.

This creates an enormous opportunity—and an urgent question for finance leaders: Are you still running last decade's billing infrastructure in a subscription economy?

Why This Matters to Your Bottom Line

Recurring billing isn't just an IT concern. It's a revenue recognition, cash flow, and customer experience issue that directly impacts your P&L. The old model of bolting billing functionality onto your ERP system made sense when one-time transactions dominated. But today's business models—subscriptions, usage-based pricing, hybrid offerings—have exposed critical limitations:

The Hidden Costs of Legacy Billing:

Manual revenue recognition processes that delay close

Inflexible pricing models that can't support experimentation

Poor customer self-service leading to higher support costs

Limited payment options causing unnecessary churn

Compliance risks with IFRS 15 and ASC 606

Modern recurring billing platforms address all of these while typically delivering faster implementations and lower total cost of ownership than traditional systems.

The SaaS Disruption is Already Underway

Gartner's analysis reveals a market dynamic that should concern any CFO running legacy billing: modern, cloud-native solutions are actively displacing high-cost incumbents. The analyst firm expects this trend to accelerate, with an intriguing twist—as expensive solutions get replaced by more efficient alternatives, the overall market size may actually shrink even as SaaS vendors capture greater market share.

Translation: the vendors offering lower-cost, more innovative solutions are winning, and the window for advantageous migration is finite.

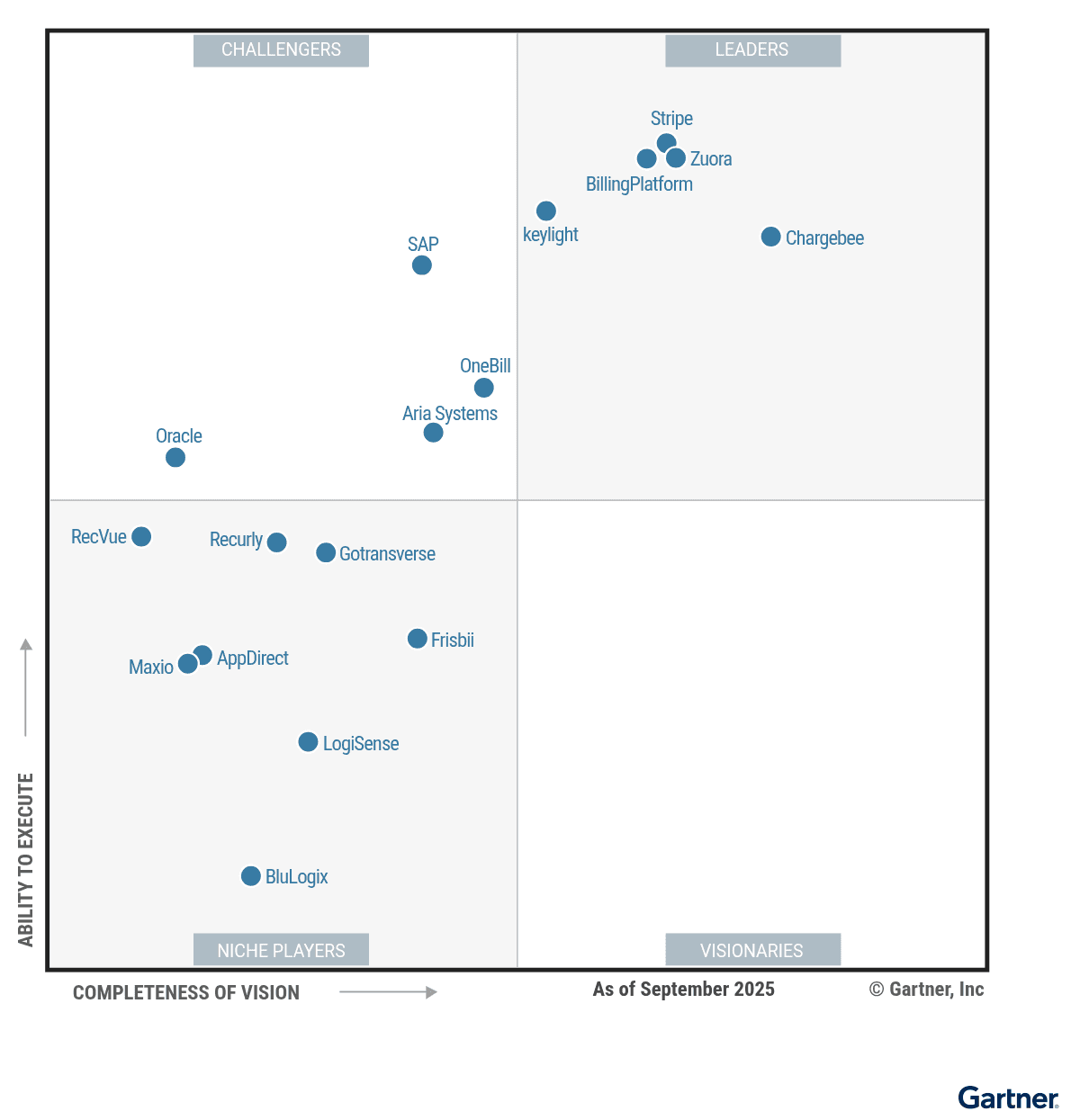

What the Leaders Are Getting Right

Gartner identified five Leaders in this space: BillingPlatform, Chargebee, keylight, Stripe, and Zuora. While each has distinct strengths, they share common characteristics that finance leaders should prioritize:

Comprehensive billing flexibility - The ability to handle one-time charges, subscriptions, usage-based pricing, and even project billing in a single platform. BillingPlatform and SAP (a Challenger) scored highest here, critical for companies with diverse revenue streams.

Revenue recognition automation - Native support for IFRS 15 and ASC 606 reduces compliance risk and accelerates close cycles. Chargebee, Oracle, and Zuora stood out in this area.

Global scalability - Multi-currency, multi-language support with local tax compliance. Stripe and SAP demonstrated the strongest capabilities for international operations.

Payment intelligence - Advanced dunning workflows and AI-driven retry logic can recover 10-15% of failed payments. Stripe's "smart retries" and flexible payment orchestration set the benchmark here.

The Strategic Implications

For CFOs evaluating this market, consider three strategic points:

1. The ERP Footprint is Shrinking

The trend is clear: companies are moving accounts receivable functionality out of their ERP and into purpose-built recurring billing platforms. Your ERP remains the system of record for the general ledger, but billing, collections, and revenue recognition increasingly live elsewhere. This isn't a downgrade—it's specialization that delivers better outcomes.

2. Industry Convergence Creates Opportunity

Gartner notes that functional requirements across industries are converging. The telecommunications-specific or utilities-specific billing solution is giving way to flexible, cross-industry platforms. This means you have access to innovation and competitive pricing that weren't available even five years ago.

3. Scale Matters, But Differently

Several smaller vendors like keylight and OneBill earned spots as Leaders or Challengers despite limited customer bases. Why? Because they're delivering superior user experiences and faster implementations. The calculation isn't simply "biggest vendor wins"—it's about functional fit, implementation risk, and total cost of ownership.

However, vendor viability remains crucial. These systems typically run for 20-30 years. Gartner weighted financial stability heavily in their evaluation for good reason.

The GenAI Reality Check

You'll see marketing around generative AI in billing platforms. Current use cases—chatbots to answer billing questions, assistants to help navigate the application—are interesting but not transformative. Gartner notes that GenAI remains a low priority for their clients compared to fundamental capabilities like ease of use, functional completeness, and predictable implementations.

Don't let AI buzzwords distract from the core evaluation criteria that actually impact your operations.

Making Your Move

If you're running legacy billing infrastructure or your ERP's accounts receivable module is straining under subscription complexity, the market has reached maturity with proven alternatives. The evaluation should focus on:

Functional completeness for your specific revenue models (usage-based, subscriptions, projects, or mixed)

Integration capabilities with your existing tech stack

Revenue recognition automation aligned with your accounting standards

Customer experience including self-service portals and flexible payment options

Vendor viability and commitment to the product line

Gartner evaluated 17 qualified vendors through extensive three-hour product demonstrations, including benchmarks on rating 1 million usage events and generating 10,000 invoices. The performance differences were stark—some vendors completed tasks in minutes while others required hours.

https://www.gartner.com/doc/reprints?id=1-2M3N7T0R&ct=251016&st=sb

The Bottom Line

The $5 billion recurring billing market isn't just growing—it's transforming. Modern SaaS solutions are delivering better functionality at lower cost than legacy systems, and the gap is widening. For CFOs, this represents both an opportunity to reduce costs and improve operational efficiency, and a risk if competitors move first.

The question isn't whether to modernize your billing infrastructure. It's whether you'll do it proactively on your timeline, or reactively when the limitations of your current system force your hand.

The vendors are ready. The technology is proven. The ROI case has been made hundreds of times over. What's your billing strategy for the next decade?