Failed payments

Payment recovery

Stripe failed payments

Gal Cegla

The $440 Billion Problem Nobody Solved

Failed payments remain the single largest source of preventable revenue loss in the subscription economy. Industry estimates put the annual cost at $440 billion globally, with involuntary churn accounting for over 50% of all subscriber losses in many verticals. Yet until recently, the solutions available were shockingly primitive: fixed-interval retry schedules, generic dunning emails, and brute-force logic that treated every declined transaction identically.

2025 changed that. AI-native recovery platforms proved they could deliver 2-4x better outcomes than legacy approaches (FlyCode). Foundation Models Entered Payments. And the first platforms began combining silent retries with AI-powered customer outreach, creating a new category of full-stack payment recovery.

This report provides an honest, data-backed comparison of the leading payment recovery platforms entering 2026. We examine recovery rates, pricing models, integration depth, compliance posture, and the emerging capabilities that will separate winners from the pack.

What Changed in 2025: Three Shifts That Reshaped the Market

1. Foundation Models Entered Payments

In May 2025, Stripe unveiled the world's first AI foundation model built specifically for payments a transformer-based architecture trained on tens of billions of transactions. Adyen's recent launch of their Uplift toolkit demonstrates the industry's commitment to AI-powered optimization, with the platform leveraging trillions of dollars worth of global data to optimize the full payment funnel

Stripe's Adaptive Acceptance, which retries legitimately declined payments in real-time, recovered over $6 billion in falsely declined transactions in 2024, with a 60% year-over-year increase in retry success rate.

This matters for the broader market because it raised the baseline. Every dedicated recovery platform now competes against a far more capable native solution than existed even 12 months ago.

2. Per-Merchant ML Proved the Next Performance Tier

While Stripe's foundation model is powerful, it optimizes for the average across millions of merchants. The next wave of performance improvement came from platforms that train custom ML models on each merchant's specific data. FlyCode, for example, builds decisioning models that analyze hundreds of data points per transaction, including customer and payment metadata, internal classifiers of error codes and messages, issuer behavior patterns, and balance-cycle signals, to create a recovery strategy unique to each business.

The difference between global models and per-merchant models is analogous to the difference between a general-purpose LLM and one fine-tuned on your company's data. Both are useful, but the fine-tuned version consistently outperforms on your specific use case. FlyCode customers report 25-40% better recovery rates than legacy solutions, with some seeing recovery rates jump from 51% to 66% in a single month (BUBS Naturals) or from 63% to 91% (Capsho).

This per-merchant approach extends beyond retry timing. FlyCode's orchestration layer routes failed payments across different payment providers to find the highest-approval path — capabilities that a single-processor model fundamentally cannot offer.

3. The Full-Stack Era Began: Retries + AI-Powered Outreach + Backup payments

The market is splitting into two tiers: platforms that only do silent retries, and platforms that combine retries with intelligent customer outreach. The data is clear: some failed payments require customer action (expired cards, lost cards, bank changes), and the platforms that coordinate retry timing with contextual outreach are recovering revenue that retry-only solutions leave on the table.

FlyCode attacks involuntary churn on three fronts simultaneously: AI-optimized retries, alternate-card-on-file, and coordinated outreach through predictive dunning emails timed to the customer's local time zone. Butter announced similar ambitions with its new Payments Score and Outreach products in January 2026, but with lower uplift of 8%-10%.

The convergence is clear: the winning platforms in 2026 will combine deep ML intelligence on when and how to retry with AI-powered outreach that knows when and how to engage the customer (FlyCode).

2026 Platform Comparison: At a Glance

The following comparison covers the platforms most actively competing in the AI-driven payment recovery space as of early 2026.

Platform | Recovery Rate | Pricing | AI Approach | Integrations | Outreach | Best For |

|---|---|---|---|---|---|---|

FlyCode | 25-40% above legacy with 5%-7% ARR lift | Pay-on-recovery | Per-merchant ML + orchestration + Visa partner | Stripe, Shopify, Recharge, Skio, Chargebee, multi-PSP | AI retries + email + AI agents + backup cards | SaaS & eCom / DTC subscription |

Butter payments | 8% - 10% above legacy | Pay-on-recovery | Global ML model | Worldpay, Braintree, Recharge | Retries + Outreach | DTC & SaaS brands |

Stripe Smart Retries | Baseline | Included in Stripe | Global ML model | Stripe only | Basic automated emails | All Stripe users |

Paddle Retain | Not publicly disclosed | Bundled with Paddle | Rule-based + ML retries | Paddle ecosystem only | Retries + cancel flows | Paddle billing users |

Vindicia Retain | Up to 15% of terminal failures legacy | Revenue share | Rule based legacy | Multi-gateway | Dynamic dunning workflows | Enterprise |

FlexFactor | Up to 20% rev / 30% decline reduction (claimed) | Revenue share (priced to cover credit losses) | Last-mile stacked retries + real-time credit-risk approval | Spreedly, OpenPath, BigCommerce, Braintree, Stripe (beta) | Invisible (no customer interaction) | One-time ecommerce checkout |

FlexPay | Up to 15% lift | Revenue share | Invisible Recovery ML | Multi-gateway | Silent retries only | High-risk merchants |

Redux | Not publicly disclosed | Performance-based | Rule based and adding retries | Stripe only | Silent retries only | Subscriptions |

Recurly | ML-optimized (no public rate) | Platform fee | ML retry scheduling | Native platform | Dunning + retries | Mid-market |

Churnkey | Not publicly disclosed. Mainly cancellation flows | Subscription-based | Adding retry on top of Stripe | Major billing systems | Cancel flows + emails | SaaS |

Chargebee Retries | Intelligent scheduling | Platform fee | Basic and smart | Chargebee | Yes | Chargebee customers |

Detailed Platform Profiles

FlyCode: The AI-Native Payment Recovery (partnered with Visa and Mastercard)

Y Combinator | Launched: 2023 | HQ: Boston

FlyCode approaches payment recovery per customer and per merchant. Rather than stacking additional retries on top of your payment processor's native logic (like Profitwell and Churnkey), FlyCode replaces the retry engine entirely with custom ML models trained on each merchant's specific transaction data. The platform analyzes hundreds of data points per failed payment — decline codes, issuer behavior, geography, card type, customer payment history, and balance-cycle signals — to determine the precise retry window and routing path most likely to succeed.

What sets FlyCode apart: FlyCode attacks involuntary churn on three fronts simultaneously: (1) AI-optimized retries with per-merchant ML models that learn continuously, (2) alternate-card-on-file routing and multi-PSP orchestration (design partner of STRIPE) that finds the highest-approval path, and (3) coordinated customer outreach — including predictive dunning emails timed to the customer's local time zone and AI-powered billing agents for complex recovery scenarios.(4) Adaptive acceptance which retries legitimately declined payments in real-time.

Direct partnerships with Visa, Mastercard and Stripe give FlyCode access to network-level insights and payment metadata that boost recovery rates while maintaining compliance-grade safeguards. This is a critical differentiator: FlyCode's models are informed by data that standalone retry engines simply cannot access.

Published FlyCode's Customers Results:

Customer | Category | Key Result | Additional Impact |

|---|---|---|---|

Capsho | SaaS (Podcasting) | Recovery rate from 63% → 91% (+44%) | Substantial ARR uplift with clear ROI |

GitBook | SaaS (Developer Docs) | 8% ARR boost | Customers in 100+ countries, enterprise-scale documentation platform |

Rewardful | SaaS (Affiliate Marketing) | 29% boost in recovery rate | 5% ARR lift, highest recovery level in 2 years |

Framer | SaaS (Web Builder) | 18%+ increase in recovery rate | 6% ARR lift, 45% increase in total recovered amount, highest in past year |

Workiz | SaaS (Field Service Mgmt) | 15% boost in payment recovery | Improved retention across service verticals |

Nav | FinTech | Uncovered hidden issues, optimized processes | "Results speak for themselves" — Head of FP&A |

Mozper | FinTech (Youth Banking) | Measurable revenue recovery improvements | Seamless integration, minimal effort to implement |

PlixLife | DTC (Health & Wellness) Partner: Shopify Recharge | 21% boost in recovery rates, 12x ROI | 9% reduction in involuntary churn |

Cymbiotika | DTC (Health Supplements, $150M+ revenue) Partner: Shopify Recharge | 22% revenue increase from recovery | 25% churn reduction, 24x ROI ($1 spent → $24 gained), baseline was ~52% |

Just Meats | DTC (Food & Beverage) Partner: Shopify Recharge | 62% increase in payment recovery | 33% reduction in churn |

Gardencup | DTC (Meal Delivery) Partner: Shopify Recharge | Recovery rate from 62% → 82% (+32%) | 20% lift in customer LTV |

Lucy | DTC (Nicotine Products) Partner: Shopify Recharge | 46% increase in payment recovery | 11% decrease in billing failures |

BUBS Naturals | DTC (Supplements) Partner: Shopify Recharge | Recovery rate from 51% → 66% in one month | Peak of 71% recovery rate in January |

The Beard Club | DTC (Grooming) Partner: Shopify Recharge | Boosted failed payment recovery | Improved subscription retention at scale |

Carpe | DTC (Personal Care) Partner: Shopify Recharge | Significant recovery improvement | Reduced involuntary churn on subscriptions |

Geologie | DTC (Skincare) Partner: Shopify Recharge | Outperformed all previously tested dunning solutions | Saves hours of work weekly vs. manual recovery |

Where FlyCode fits:

Cross-customer patterns: FlyCode customers span SaaS, DTC, FinTech, and eCommerce — from early-stage startups to $200M+ revenue brands like Cymbiotika and Framer (In August 2025, Framer that valued at $2 billion, Nav the financial platform and the best apps in the App store like: Riverside and Simply.

Partnership with the card networks: FlyCode partnered with Visa (in 2024) and with Mastercard (in 2026) to deepen the level of data models.

Recovery rate improvements range from 17% to 62%, churn reductions of 14-33%, and ARR lift of 5-9%. Multiple customers report 12-24x ROI. Results are consistent across both Stripe (SaaS), Chargebee (SaaS) and Shopify Recharge, Skio and Loop (DTC) integrations, with customers going live in minutes and seeing measurable impact within 1-2 billing cycles.

Pricing: Pay-on-recovery only. No seats, no minimums. FlyCode charges only on dollars it actually recovers above your base line, creating perfect incentive alignment with merchants.

Integration: Zero-integration via Stripe app, Chargebee app, Recharge App, Skio app, Loop app. Also supports Shopify and multi-PSP orchestration across different payment providers.

Best for: SaaS and AI subscription businesses on Stripe, Chargebee, customer build or Shopify eCommerce that want a full-stack recovery solution combining intelligent retries with coordinated outreach, without the enterprise sales cycle.

Butter Payments: DTC Recovery focusing on retries

Founded: 2019 | HQ: San Francisco

Butter built its reputation on ML models that treat each failed payment individually rather than applying batch retry logic. In 2025, Butter reported recovering 12% more subscription revenue year-over-year and added new AI recovery models to its platform. The company serves major DTC and enterprise brands including The Athletic, Fabletics, and Savage X Fenty.

Strengths: Deep DTC expertise, enterprise client base, dedicated support teams

Considerations: Historically focused on eCom, Braintree, and Recharge. Enterprise positioning means potentially longer sales cycles and higher price points for smaller SaaS companies.

Best for: Mid-market to DTC and subscription brands with high transaction volumes seeking a retries product.

Stripe Smart Retries: The Baseline

Stripe Smart Retries uses ML trained on Stripe's massive global transaction data to optimize when and how to retry failed payments. It's free for all Stripe Billing users and requires zero additional setup. Stripe claims a 9x ROI on Stripe Billing costs through recovered revenue, and that recovered subscriptions continue for an average of seven more months.

The limitation is fundamental: Smart Retries are a generalist solution optimized for Stripe's entire merchant base, from solo freelancers to Fortune 500 companies. It cannot adapt to the specific patterns of your business the way a dedicated per-merchant ML model can (FlyCode). It also operates only within the Stripe ecosystem.

Strengths: Free, zero setup, trained on enormous dataset, good baseline for all Stripe users.

Considerations: Cannot be customized per merchant. Should be considered the floor, not the ceiling.

Best for: Any Stripe user as a starting point. Businesses that want more should layer a dedicated solution on top.

Baseline: FlyCode is using the Stripe payment recovery as baseline and show a boost of 23% in recovery rate for AI companies, a 27% for B2C companies, 19% boost with FlyCode for B2B companies and 26% for DTC subscriptions.

According to Stripe this is how to identify causes of failed payments in your business:

Taking steps to prevent and respond to failed payments is important, but properly addressing these issues depends on knowing why failed payments are happening in your business in the first place. Here’s a step-by-step process to help you figure out the root causes of your failed payments:

Check the decline code: On an individual level, the first step in determining what caused a failed payment is to check the decline code provided by your payment processor. A card decline code is typically a two-digit, alphanumeric error code that explains why a card transaction was declined.

Examine your payment gateway: If you’re investigating multiple failed payments, looking at your payment gateway can often provide answers. Conduct a thorough audit of your gateway integration to compile data about what types of transactions have been failing. An issue could become quickly apparent, but if not, gather as much information as possible.

Review fraud prevention settings: Because fraud detection and prevention tools can sometimes flag legitimate payments, review each setting to determine whether any are set too strictly or may have been erroneously marking payments as suspicious.

Analyze the payment data: Look closely at the data you compiled from your payment gateway and fraud prevention software to try to determine whether there are any factors affecting your business’s payments. It could be a certain payment method, transactions from a specific region, or payments during a particular time of day that are more likely to fail. If a pattern emerges, that’s likely your answer.

Paddle Retain (formerly ProfitWell Retain): The Bundled Play

Paddle acquired ProfitWell for $200M in 2022, and Retain is now integrated into Paddle's merchant-of-record billing platform. The product combines retry logic with cancel flow optimization and subscriber retention. As part of Paddle, Retain benefits from being bundled with billing, tax management, and fraud prevention.

However, Retain's technology was originally built in 2012 and operates on a rule-based foundation with fixed-interval retry schedules. It stacks additional retries on top of Stripe's native system rather than replacing it. For businesses already committed to Paddle as their billing platform, Retain is a natural add-on. For those seeking best-in-class recovery performance, the legacy architecture may limit results.

Strengths: Bundled with full billing stack, cancel flow optimization, established brand.

Considerations: Legacy technology, locked into Paddle ecosystem, no per-merchant ML. Recovery performance lag AI-native alternatives.

Auth rate: Profitwell added 3-5 retries to Stripe, on the same time that Stripe are doing retries. This can reduce the recovery rate for merchants for over retrying.

Best for: Businesses already using Paddle Billing who want integrated retention tools without adding another vendor.

ProfitWell is a Paddle feature. FlyCode is a Payment recovery powerhouse

Learn more: FlyCode vs. ProfitWell by Paddle Retain

Churnkey: The Voluntary Churn

Founded: 2021 | HQ: United States

Churnkey positions itself as a Voluntary churn and cancellation flow product rather than a pure payment recovery tool. Its Intelligence Suite combines basic payment recovery with cancel flow optimization, pause subscriptions, feedback , and retention analytics. The platform claims to have retained nearly $550 million in additional LTV for its customers to date.

On the payment recovery side, Churnkey offers basic retries stacked on top the Stripe retries, outreach dunning (email, SMS, and in-app), and a distinctive "payment wall" feature that restricts access to product features until customers update their payment method — reportedly adding 3% to recovery rates. Their 2025 State of Retention report showed a 11% recovery rate across all involuntary churn detected on their platform, with a 32% recovery rate from dunning campaigns alone. Churnkey also recently launched A/B testing for recovery campaigns, allowing businesses to experiment with copy, timing, subject lines, and retry logic to optimize performance.

Strengths: Cancelation platform addressing both voluntary churn, strong cancel flow personalization (discounts retained 13% of would-be cancellers, pauses rescued 9%), in-app payment walls, no-code setup, and dedicated AI-powered feedback analysis. Claims 32% voluntary churn reduction and 13% payment recovery rates for qualifying customers.

Considerations: Primarily serves SaaS and subscription businesses with monthly churned revenue above $500. Less focused on multi-PSP orchestration or payment routing optimization. Recovery is one basic module among many, not the singular focus of the platform.

Payment recovery: Basic rule based on top of Stripe. Churnkey doesn't replace Stripe model. Chrunkey product adding 3-5 retries on top of Stripe on the same time of Stripe retries which limit the recovery rate and may lower auth rate.

Best for: Self-serve SaaS companies that want a single platform to address both voluntary cancellations and involuntary payment failures, with built-in analytics and feedback tools. You can keep your cancel-flows with Churnkey and pick FlyCode for payment recovery

Read more: Churnkey is for cancellations. FlyCode is a payment optimization platform

Vindicia Retain: The legacy system that is doing only last mile recovery

Vindicia has been in the payment recovery space for over 20 years and claims the ability to recover up to 10% of terminally failed transactions. Its basic algorithms are trained on historical transactions, and its enterprise positioning comes with PCI-DSS Level 1 Version 4 compliance, GDPR certification, and comprehensive security infrastructure.

The trade-off is clear: Vindicia is purpose-built for legacy enterprises with complex billing stacks. Implementation can involve $5,000-$50,000 in setup costs, longer deployment timelines, and revenue-share pricing that makes sense at scale but may not for smaller subscription businesses.

Strengths: Deepest dataset in the market, multi-gateway support, enterprise-grade compliance, 20+ years of payment intelligence.

Product: Vindicia is handling retries after you already tried to save the payment for awhile. It means they only add extra retry attempts at the end of your existing flow. This approach isn't recommended long-term because it can actually lower your authorization rates for stacking retries. FlyCode for example, manage the entire payment recovery flow from the start, not just the long tail.

Considerations: Legacy pricing and deployment complexity. May be overkill for SMB or mid-market SaaS companies.

Best for: Large enterprise subscription businesses with complex billing that need the deepest analytics and compliance certifications.

FlexFactor: Last-Mile Retries Plus a Credit-Risk Approval Layer

HQ: Dover, DE and Bristol, UK

FlexFactor (the AcceptIQ platform) is often filed next to retry tools, but it is really two products bolted together, and the marketing emphasizes the more novel half. Understanding both halves matters before you sign.

Half one: last-mile stacked retries. Like Churnkey, Paddle Retain, and Vindicia, FlexFactor adds its own retry attempts on top of the retries you already run. This is the same stacking pattern flagged throughout this report: when two systems retry the same card on overlapping schedules, issuers can interpret it as uncoordinated over-retrying, which can suppress your authorization rate over time. Stacked retries can recover a few extra transactions in the short term while quietly degrading the auth rate on everything else. A dedicated engine that replaces the retry logic (FlyCode, Butter) avoids this by design.

Half two: real-time decline approval with credit risk. This is the genuinely different part. For a transaction the issuer has declined, FlexFactor can step in and approve it anyway, fronting the money so the merchant completes the sale on the spot, then carrying the credit risk itself. Mechanically, this is closer to a lending or transaction-guarantee product than to dunning or recovery.

The thing to understand before you sign: the pool of transactions FlexFactor approves is, by definition, the transactions a bank already declined. Issuers decline for reasons — insufficient funds, over-limit, suspected fraud, closed accounts. Approving the declined pool means underwriting exactly the slice of customers the issuer's own risk models flagged as highest-risk. That is textbook adverse selection: you are not getting a random sample of customers, you are getting the worst-scoring ones. FlexFactor prices its revenue share to cover the expected credit losses on that pool, which means the merchant ultimately pays for the bad debt, bundled into the fee. For genuinely false declines (a good customer wrongly rejected), this can be a real win. For the rest of the declined pool, the economics are doing a lot of quiet work.

Strengths: Genuinely novel approach to one-time checkout declines, fully invisible to the customer (no prompts or re-entry), covers both one-time (CIT) and subscription (MIT) transactions, fast one-click integration through pre-integrated gateways. Claims up to 20% annual revenue increase and up to 30% reduction in decline rates.

Considerations: The stacked-retry half carries the same auth-rate risk as Churnkey and Vindicia. The approval half is a credit-risk product underwriting your worst-scoring (declined) traffic, with revenue share priced to absorb the losses. Center of gravity is one-time ecommerce checkout rather than subscription recovery.

Integrations: Spreedly, OpenPath, BigCommerce, Braintree, and a native Stripe app in beta.

Best for: High-volume one-time ecommerce where a meaningful share of declines are genuine false positives and the merchant is comfortable with a credit-risk intermediary in the checkout flow. For subscription (recurring) payment recovery, a dedicated engine like FlyCode goes deeper without stacking retries or adding a lending layer.

Other Platforms

Slicker :offers a five-minute setup with pay-for-success pricing and claims 2-4x improvement over native billing logic. Strong multi-gateway support across Stripe, Chargebee, Recurly, and Zuora. Still in growth phase

FlexPay specializes in high-risk merchant categories with its Invisible Recovery technology that resolves soft declines without customer visibility. Strong compliance posture and mid-market to enterprise focus.

Recurly and Chargebee offer integrated retry logic as part of their subscription management platforms. Good for businesses already on their billing stack, but recovery is a feature rather than the core product.

Decision Framework: How to Choose

Choosing a payment recovery platform is not a one-size-fits-all decision. The right platform depends on your billing stack, transaction volume, growth stage, and how you prioritize recovery performance versus simplicity. Here are the dimensions that matter most:

1. Per-Merchant ML vs. Global Models

The single biggest performance differentiator. Platforms like FlyCode and Butter train custom models on your specific transaction data, issuer patterns, and customer behavior. Global models (Stripe Smart Retries, Recurly) optimize for the average across millions of merchants. If your business has distinct payment patterns — and most do — per-merchant ML will outperform.

2. Replaces vs. Stacks the Retry Engine

A critical and often-overlooked dimension. Some platforms replace your retry logic with one coordinated decisioning layer (FlyCode, Butter). Others stack their retries on top of your existing flow (Churnkey, Paddle Retain, Vindicia, and FlexFactor's retry half). Stacking means two systems retrying the same card on overlapping schedules, which issuers can read as uncoordinated over-retrying and which can suppress your authorization rate over time. Always ask whether a platform supplements or replaces native retry logic.

3. Software Recovery vs. Credit-Risk Product

Most tools here are pure software: they recover the legitimate payment through better timing, routing, or outreach, and take on no balance-sheet risk (FlyCode, Butter, Churnkey, Stripe). FlexFactor's approval layer is different — it fronts the money on declined transactions and carries the credit risk, underwriting the worst-scoring (declined) pool with revenue share priced to cover the losses. That can help for genuine false declines at one-time checkout, but it is a fundamentally different commercial model from software recovery, and the merchant absorbs the credit losses through the fee.

4. Integration Breadth

Are you Stripe-only, or do you run multiple payment processors? Platforms like FlyCode, Vindicia, and FlexPay support multi-PSP orchestration, routing failed payments through the highest-approval path across different processors. Single-processor platforms (Stripe Smart Retries, Redux) cannot do this. For businesses processing payments through multiple gateways, orchestration capability is essential.

5. Pricing Alignment

Models exist on a spectrum: pay-on-recovery (FlyCode, Butter), revenue share (Vindicia, FlexPay, and FlexFactor — though FlexFactor's is priced to cover credit losses, not just recovery), and platform-bundled (Stripe, Paddle, Recurly). Pay-on-recovery creates the strongest incentive alignment: the platform only earns when you do, with no credit-loss premium baked in.

6. AI Architecture Depth

Not all "AI-powered" recovery is equal. At one end of the spectrum, Stripe's Payments Foundation Model uses self-supervised transformer architecture trained on tens of billions of transactions — a genuine technical breakthrough. At the other end, some platforms label basic rule-based retry schedules as "AI." The questions to ask: Does the platform train models on your specific merchant data? Does it continuously learn from each transaction outcome? Can it route across multiple processors? Does it coordinate retries with outreach? Platforms with deeper AI architecture (FlyCode's per-merchant ML, Stripe's foundation model, Butter's patented models) will consistently outperform those running fixed schedules with an AI marketing label.

The best way to evaluate any recovery platform: Start with your baseline. Know what percent of MRR is lost to involuntary churn, by payment method, issuer, country, and decline code. Then pilot side by side and let the data decide.

Involuntary Churn and failed payments Rates: The Numbers Behind the Problem

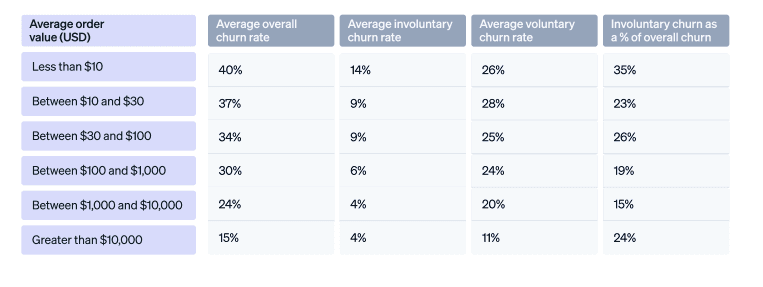

By Average Order Value

Involuntary churn rates decrease as subscription prices increase (from the Stripe churn report):

Less than $10: 14% involuntary churn rate

$10-$30: 9% involuntary churn rate

$30-$100: 9% involuntary churn rate

$100-$1,000: 6% involuntary churn rate

$1,000-$10,000: 4% involuntary churn rate

Greater than $10,000: 4% involuntary churn rate

Lower-priced subscriptions face higher involuntary churn, likely because customers using these services may have less reliable payment methods or tighter cash flow.

By Payment Method

The payment method customers use dramatically impacts involuntary churn rates:

Prepaid cards: 23% involuntary churn (highest risk)

Debit cards: 11% involuntary churn

Credit cards: 6% involuntary churn (lowest risk)

Prepaid cards are nearly 4x more likely to experience involuntary churn compared to credit cards, primarily due to insufficient funds.

By Business Model

B2C businesses: 9% involuntary churn rate

B2B businesses: 6% involuntary churn rate

B2C businesses face higher involuntary churn rates, likely due to consumers experiencing more payment issues like insufficient funds and card declines.

By Industry

Involuntary churn rates vary significantly across industries:

Furniture: 13%

Digital goods: 11%

Business services: 10%

Education: 10%

Personal services: 9%

Merchandise: 9%

SaaS: 8%

Travel and lodging: 8%

Leisure: 6%

Insurance: 3% (lowest)

The Composition of Total Churn

Involuntary churn represents a significant portion of overall customer churn:

Prepaid card users: 51% of their total churn is involuntary

Debit card users: 28% of total churn is involuntary

Credit card users: 18% of total churn is involuntary

B2C businesses: 24% of overall churn is involuntary

B2B businesses: 16% of overall churn is involuntary

How to pick a payment recovery tool for failed payments?

You need to ask a few questions: 1. Does the product simply stack retries, or does it actually use its own proprietary model? 2. Does the product only handle the "last mile"? Some solutions only add extra retry attempts at the end of your existing flow. 3. Do you only pay for incremental results above your current recovery rate? 4. Is the product just a fancy email solution for failed payments?

What is the difference between Stripe Smart Retries and a dedicated payment recovery platform like FlyCode?

Stripe Smart Retries uses a global ML model trained across Stripe's entire merchant base to optimize retry timing — and it's free for all Stripe Billing users. However, it optimizes for the average across millions of businesses and cannot adapt to your specific transaction patterns. Dedicated platforms like FlyCode train per-merchant ML models on your individual data — including decline codes, issuer behavior, and customer payment history — and can route failed payments across multiple processors to find the highest-approval path. FlyCode customers report 25-40% better recovery rates than legacy solutions. Think of it as the difference between a general-purpose AI and one fine-tuned on your company's data: Stripe is a strong baseline, but per-merchant ML consistently outperforms on your specific use case.

How much revenue can a payment recovery platform actually recover?

Results vary by business, but published benchmarks across leading platforms show meaningful impact. FlyCode customers report recovery rate improvements of 15-62%, churn reductions of 9-33%, and ROI of 12-24x. Specific examples include Cymbiotika (22% revenue increase, 24x ROI), BUBS Naturals (recovery rate from 51% to 66% in one month), and Capsho (63% to 91% recovery). Stripe's Adaptive Acceptance recovered over $6 billion in falsely declined transactions in 2024. Churnkey's 2025 data showed 70% of all involuntary churn detected was recoverable. The key variable is your current baseline — businesses still relying on native retry logic or fixed-interval schedules typically see the largest gains when switching to an AI-native solution.

What should I look for when choosing a payment recovery platform?

The pros are strategic redundancy: if one gateway fails because of a cyberattack, technical issue, or routine maintenance, another can take over so transactions can continue without interruption.

Global market penetration: each payment gateway supports different currencies, regions, and local payment methods.

Competitive routing: by employing advanced routing algorithms, businesses can dynamically select the most cost-effective gateway for each transaction based on real-time fee assessments.

Approval ratios: Different payment gateways have different relationships with financial institutions and their underlying technology, which affect transaction approval rates.

Consumer preferences: different consumers have divergent preferences and trust levels with various payment methods and gateways.

Risk mitigation and compliance: because different gateways often have varied security features and adhere to regional regulations, such as GDPR in Europe or CCPA in California, using multiple gateways allows businesses to diversify their risk and maintain continuous compliance with regulatory standards across borders.

How quickly can a payment recovery platform show results?

Most modern platforms deploy far faster than legacy enterprise solutions. FlyCode offers zero-integration deployment via the Stripe app and customers typically go live in minutes, with measurable recovery impact within 1-2 billing cycles. Slicker also advertises a five-minute setup. By contrast, enterprise platforms like Vindicia may involve $5,000-$50,000 in implementation costs and longer deployment timelines. The fastest way to evaluate any platform is to run a controlled A/B test: split your failed payments between your current solution and the new platform, then compare net recovered revenue and post-recovery subscription tenure over 30-60 days.

What is the difference between voluntary and involuntary churn, and why does it matter for recovery?

Voluntary churn happens when customers actively choose to cancel — they're unhappy with the product, found an alternative, or no longer need the service. Involuntary churn happens when customers lose access because a payment fails, not because they wanted to leave.

Can I use a dedicated payment recovery platform alongside Stripe Smart Retries, or do I have to choose one?

It depends on the platform. Some solutions like Paddle Retain and Churnkey stack additional retries on top of Stripe's native logic, which can lead to redundant retry attempts and potentially higher decline rates with issuers. FlyCode takes a different approach, it replaces Stripe's retry engine entirely with its own per-merchant ML models, ensuring there's no conflict between competing retry schedules. This is an important technical distinction: layering retries on top of retries can actually hurt performance if the systems aren't coordinated, because issuers may flag excessive retry attempts. When evaluating any platform, ask specifically whether it supplements or replaces native retry logic, and whether it coordinates retry timing across all systems to avoid redundant attempts. The best outcomes come from a single intelligent decisioning layer that owns the full recovery strategy for each failed payment.